.jpg)

Before diving into the mechanics of international wire transfers, let’s ask some essential questions: Why do people send money across borders? What do they need to know? Are there unique aspects of wire transfers? Who can you trust, and what should you look for when choosing a remittance provider?

This is the first in a series of five articles that will answer these questions and more. By the end of the series, you’ll be a wire transfer expert and might even discover a better alternative. So, let’s get started.

A wire transfer, commonly used to describe both traditional bank wires and international money remittances, is an electronic method of sending money, either domestically or internationally. Traditional bank wire transfers use a specific network to move money from one bank to another. New money transfer methods are now available, which you can think of as “digital wire transfers.” These new methods don’t rely on the traditional bank wire transfer network, and can offer more options for sending money. The time it takes to complete a transfer can vary significantly—ranging from a few seconds to several days—depending on factors such as the chosen transfer method, the destination country, and the financial institutions involved.

There are several ways to send money internationally via wire transfer, each with pros and cons. Let’s explore some popular methods.

Using a bank is the traditional method for wire transfers and often the first option people consider. Here’s what you should know:

Something interesting happened during the COVID-19 pandemic. It contributed to the accelerated adoption of digital financial services, including remittance platforms like Remitly, Wise, and WorldRemit as alternatives to traditional wire transfers, which you can think of as digital wire transfers. Remittance platforms offer ways of sending money abroad that don’t rely on the traditional wire transfer process. These apps remain popular in the post-pandemic era for their convenience and efficiency.

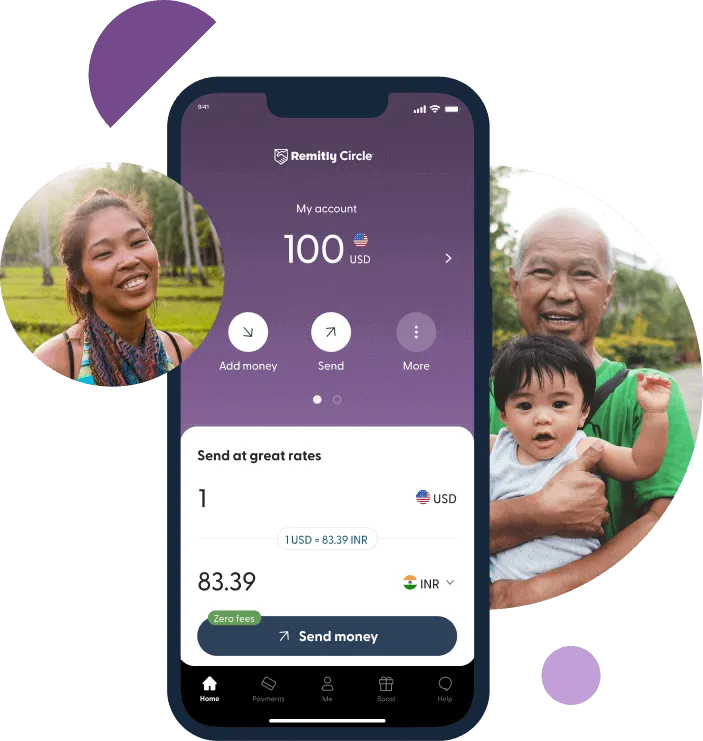

Remitly Circle offers an innovative solution for managing remittances. It allows you to store and share funds with loved ones worldwide through designated sub-accounts. These accounts give recipients direct access to the shared sub-account and, thus, they are able to be active participants in financial management. Of course, you can always use Remitly Circle to send money to your non-US bank account, similar to a bank wire transfer. In many ways, Remitly Circle represents the next evolution in remittance services.

Banks, digital apps, and Remitly Circle each have unique strengths for cross-border money transfers. Banks offer unmatched security and capacity for large transfers but are costly and less flexible. Digital apps provide affordability, speed, and convenience but depend on technology and may have transfer limits. Remitly Circle revolutionizes remittances with shared accounts, eliminating fees and introducing USD storage.

Are you curious about placing a wire transfer, sending money using a digital app, or sharing a Remitly Circle sub-account with your family? Stay tuned for the next article, where we’ll provide a step-by-step guide to mastering cross-border financial management.